Revaluation is mandatory (NCGS 105-286), so we don’t really have a choice. However, revaluation would still be a good practice, even if it weren’t mandatory.

Revaluation maintains equity of assessment.

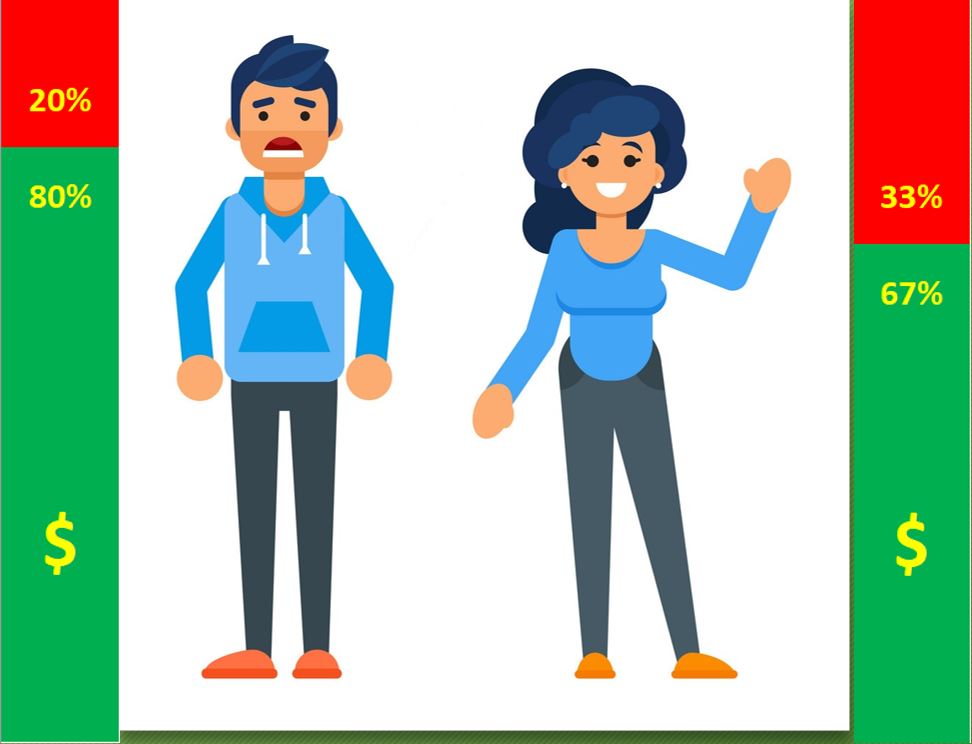

Let’s say that two people, call them “Joe” and “Jane” each purchase a home. Joe purchases his home for $200,000 and is assessed at $200,000. Jane purchases her home for $200,000 and is assessed at $200,000. Joe and Jane are being taxed equitably.

Fast-forward to 6 years later. Joe’s home has appreciated to $250,000 but he is still being assessed at $200,000, or 80% of his home’s true value. Jane has made a better purchase and her home is now worth $300,000, but she is still being taxed at $200,000, or 67% of her home’s true value. Joe is being taxed at 80 cents-on-the-dollar while Jane is only paying 67 cents-on-the-dollar. This is not equitable.

The solution is to revalue. Now Joe’s home worth $250,000 is taxed at $250,000 and Jane’s home worth $300,000 is taxed at $300,000. Both are now paying dollar-for-dollar. Equity is restored.

Revaluation maintains equity between property types.

Personal property (planes, boats, trailers and mobile homes), business personal property (machinery, equipment, furniture, fixtures, computers, and supplies), public service companies (railroads, electric, gas, telecommunication, and shipping), and registered motor vehicles are revalued every year. This means that they are always at-or-around 100% valuation (dollar-for-dollar).

For every year that passes from the time real property is valued, the market moves on (and usually up). After a number of years, real property owners may be paying 70 or even 50 cents-on-the-dollar, while all other property owners are still at 100%. This is not equitable.

Revaluations set real property owners and owners of other types of property back on the same footing at 100% assessment-to-value (or dollar-for-dollar) taxation.

Revaluation maintains transparency of assessment.

Property values change over time. Without revaluation, it would be hard to tell if your value is correct.

For example, let’s say that a county last revalued in 1950. You purchase a new house for $225,000 and the tax assessor sets a value of only $25,000 (in 1950 dollars). Is this too high? Is this too low? You probably can’t tell, and that means you can be valued incorrectly for years and have no idea. With a revaluation, that $25,000 in 1950 dollars may turn out to be $295,000 in 2022 dollars (and you would know it was too high and would appeal).

“Isn’t one of the reasons to raise taxes?”

Revaluations are not useful in raising taxes. At revaluation, the Board of County Commissioners must publish the tax rate that would undo the increase in property value (this is called the revenue neutral tax rate). Then, if they chose a rate higher than this published rate, everyone knows the Commissioners raised their taxes. On the other hand, if they chose a rate lower than the published rate, everyone knows the Commissioners lowered their taxes.

Just like in any other year, it is the Commissioners (and City/Town Councils) who control if taxes go up or down. Increasing values at revaluation only leads to lower tax rates to compensate.

“If my value goes up, won’t my taxes go up?”

If a tax rate is adopted which undoes the value increase (see above), then it all comes down to how you compare with your neighbor. If your value goes up more than average, your bill will probably go up. If your value goes up less than average, your bill will probably go down. So, if the average value increases by 75%, but your value increases by only 65%, you could see a decrease in your bill (even through you just went up 65%).

It’s worth noting that the tax burden shifts away from real property owners and onto owners of other property types between revaluations (see “equity between property types,” above). At reval, this shifts back, so there may be a small increase to the average real property bill coming from other property types (and not an increase in taxes collected).